Tips are not subject to Value-Added-Tax (VAT) as they are considered voluntary payments between the customer and service worker. HMRC guidance classifies voluntary tips and discretionary service charges as outside the scope of VAT, regardless of whether they are paid in cash or by card. However, mandatory service charges added to a bill are part of the taxable supply and attract VAT at the standard rate of 20%.

Businesses avoid VAT on tips by keeping them genuinely voluntary and separate from goods or services. Mandatory service charges must be included in VAT returns, while discretionary service charges remain exempt if customers can choose to remove or change them.

Tips are taxable as employment income and subject to Income Tax. National Insurance Contributions depend on how tips are distributed. Direct cash tips are free from NICs, but employer-controlled or card tips attract PAYE deductions. Using a compliant tronc system or digital tipping platforms like URocked allows businesses and employees to avoid NICs legally.

URocked’s tipping software ensures compliance with UK tipping laws by automating tip distribution, separating funds from business income, maintaining transparent records, and guaranteeing full payment of tips to workers.

No, tips are not subject to Value-Added-Tax (VAT) as they are considered voluntary payments between the customer and service worker. In the UK, customers do not pay VAT on tips as long as they are voluntarily given. Tips are voluntary payments and are not considered part of the supply of goods and services. The HMRC, outlined in their Guidance on tips, gratuities, service charges and troncs, considers tips outside the scope of VAT when genuinely freely given. This applies to all hospitality venues, including restaurants, cafés, and bars, regardless of whether the tip is paid in cash or by card.

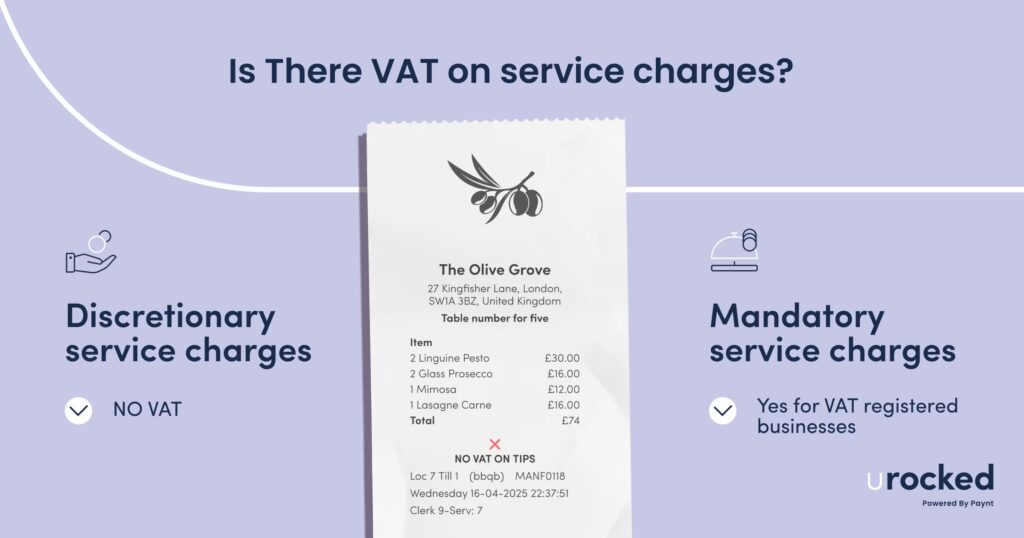

In restaurants, there is no VAT on tips or discretionary service charges. Tips and discretionary service charges are voluntary payments in recognition for good service. Customers receiving a restaurant bill should not have VAT applied to any tip or discretionary service charge. For workers there should be no deductions for VAT on tips earnt. Restaurants that are VAT registered may opt to charge mandatory service charges which require customers to pay a fee in addition to their goods and services. Mandatory service charges incur VAT in restaurants for VAT registered businesses.

In the UK, customers and businesses do not need to avoid VAT on tips because they are not subject to VAT, provided they are genuinely voluntary. Businesses can avoid charging and accounting for VAT on tips by ensuring all gratuities remain genuinely voluntary. A tip is not considered part of the goods and services supplied by a business. Businesses should not apply VAT on tips and should not account for VAT on tips in their VAT returns.

Businesses should make the distinction between a tip and a mandatory service charge. Mandatory service charges which are fees added to the bill where there is an obligation to pay. Mandatory service charges are subject to VAT at the standard rate of 20%.tment of service charges follows separate rules which affect whether VAT should be charged.

Businesses and workers can legally avoid National Insurance Contributions (NICs) on tips by using a compliant, independent ‘tronc’ system or using digital tipping platforms that separate tips from business transactions. Businesses using an independent tronc or digital tipping platform do not pay employers’ NICs. Workers who receive tips through a tronc or with a digital tipping platform are not subject to employee NICs.

A tronc is a separate arrangement for pooling and distributing tips, managed by a person known as a ‘troncmaster’. A troncmaster must be independent from the employer and have no business ownership stake. Cashless tipping platforms like URocked process tips directly to staff without employer involvement also qualify for NIC exemption as they separate tips from the business.

Staff receiving tips through these platforms avoid paying employee NICs on their tip income, while employers avoid employer NICs on the same payments. Payments through properly operated troncs or qualifying digital platforms remain exempt from NICs but are still subject to PAYE Income Tax deductions.

Yes, there is VAT on mandatory service charges at the standard rate of 20% for VAT registered businesses. There is no VAT on discretionary service charge. A mandatory service charge is a fee added to the bill where there is an obligation to pay. Mandatory service charges most commonly apply in the hospitality industry such as restaurants, hotels, cafes and other service industries. This is not to be confused with property service charge.

Mandatory service charges differ from tips because businesses impose them on customer bills. They are an obligation to pay and part of the taxable supply of goods or services. Businesses include mandatory service charges in their VAT calculations and remit the tax to HMRC through regular VAT returns. Customers pay VAT on service charges as part of the total bill amount, unlike voluntary tips which remain outside VAT scope.

VAT and all statutory tax are deducted from service charges before being distributed to employees. Restaurants typically collect mandatory service charges and share them between eligible staff through team pooling systems. The net portion of mandatory service charges, after VAT deduction, is allocated to the team pool and distributed to staff according to the business’s tip and service charge policy. Each employee’s allocated service charge is subject to Income Tax and National Insurance Contributions at standard rates.

To calculate VAT on a mandatory service charge, follow the steps below:

Step 1: Identify the mandatory service charge amount on the customer’s bill. This charge is a percentage of the total bill based on your business preference. They are typically 10%, 12.5%, 15% or 20% and automatically added and cannot be refused by the customer.

Step 2: Add the mandatory service charge to the subtotal of goods or services provided. The VAT calculation must be applied to this combined total as the service charge forms part of the taxable supply.

Step 3: Calculate the VAT on the combined total using the current UK standard rate of 20%. Apply the formula: Combined Total × 0.20 to determine the VAT amount due.

Step 4: Present the VAT separately on the customer’s invoice. The bill must clearly show the subtotal, mandatory service charge, combined total, VAT amount, and final total including VAT.

Example: A restaurant bill totalling £100 with a 10% mandatory service charge (£10) creates a combined total of £110. The VAT calculation becomes £110 × 0.20 = £22, resulting in a final bill of £132 including all charges and VAT.

No, there is no VAT on discretionary service charges as they are treated as voluntary gratuities that fall outside the scope of VAT. A discretionary service charge is a fee added to the bill that the customer can choose to pay or not to pay. The customer’s voluntary choice makes them equivalent to tips rather than part of the taxable supply of goods or services. HMRC considers these charges as personal payments to staff members rather than additional consideration for the business transaction, which exempts them from VAT liability.

Discretionary charges must be genuinely optional, clearly presented as such on menus and bills, and customers must retain complete freedom to remove or adjust the amount without consequence. This distinction separates discretionary service charges from mandatory service charges, which are automatically added to bills and subject to VAT at the standard rate of 20%. Businesses must ensure discretionary charges are properly identified and processed to maintain their VAT-exempt status under UK tax regulations.

Yes, tips are taxable and subject to income tax in the UK. All tips received are classified as employment income under UK tax law, making them liable for Income Tax in all circumstances. For tips received under employer control National Insurance Contributions (NICs) are due for both the employer and the employee. There is no VAT on tips in the UK.

National Insurance Contributions depend on how tips are distributed to staff. Tips paid directly from customer to employee are subject to Income Tax but no National Insurance Contributions. The employee is responsible for declaring these tip earnings to HMRC. Tips under employer control such as card tips added to bills are taxable tips and subject to Income Tax, employee NICs and employers NICs. The employer is responsible for operating PAYE, deducting tax and National Insurance deductions.

Tips distributed through an independent tronc system are subject to Income Tax for employees. For both employees and employers no National Insurance Contributions are due on tips using an independent tronc system.

Tips are subject to income tax in the UK with National Insurance Contributions for employer and employee if tips are under employer control. HMRC applies different taxation based on how they are paid and distributed. Tips received as cash, processed through card payments, paid digitally, distributed via tronc systems, or given as gift vouchers will be subject to different tax obligations.

Cash tips paid directly from customers are subject to Income Tax but exempt from National Insurance Contributions (NICs). When employers control the distribution of cash tips, PAYE applies, and both Income Tax and NICs are deducted automatically.

Card tips processed through business payment systems fall under employer control, making employers responsible for PAYE deductions for Income Tax and NICs. Card tips processed through tipping solutions such as URocked are not subject to employer or employee NICS. Digital tips follow the same principle: when paid directly by customers, they must be declared via Self Assessment; when distributed by employers, PAYE and NIC deductions apply.

Tronc tips are distributed through an independent pooling system managed by a troncmaster. The troncmaster operates PAYE for Income Tax but no NICs apply for either party. Gift vouchers received outside employer control are taxable as employment income at their cash equivalent but exempt from NICs. If controlled by employers, the voucher’s value is processed through PAYE with both Income Tax and NICs applied.

Tips are not taxable as business income, are not subject to VAT but are subject to employers’ National Insurance Contributions on tips if they are under employer control. Tips belong to employees as additional compensation for their services and do not form part of business revenue or profit calculations. All tips that are received by the employer and where the employer has significant control in how tips are distributed are employer controlled tips. All tips under employer control are subject to employers National Insurance Contributions. Employers must pay employer National Insurance Contributions at 15% on earnings above £5,000 per year from 6 April 2025. These earnings include workers salaries and tips they receive as part of their job.

Businesses are responsible for operating PAYE (Pay As You Earn). Businesses receiving tips must process these amounts through their payroll system and deduct Income Tax and National Insurance Contributions via PAYE before distributing tips to staff.

Use the URocked Tipping App to record tips for tax purposes. URocked’s Tipping App provides a comprehensive digital solution for tracking all tip income required for HMRC compliance and Self Assessment declarations.

URocked Tipping App offers several features that make it an excellent choice for tip recording. The app maintains a user-friendly interface that simplifies the process of logging tip amounts throughout the working day. All digital tips received directly from customers or as part of pooled arrangements are automatically recorded within the system.

The app captures essential transaction details including dates, amounts, payment methods, and tip sources for complete audit trails. URocked’s Tipping App ensures compliance with UK tax law by maintaining records in formats acceptable to HMRC for Self Assessment reporting. The platform generates easy-to-export reports that streamline the Self Assessment process, reducing the administrative burden of manual tip calculation and declaration.

URocked’s tipping software ensures compliance with UK tipping laws by automatically separating tips from customer bills and distributing funds directly to staff members without ever entering the business’s accounts. In the UK, URocked complies with the Employment (Allocation of Tips) Act 2023 by passing 100% of tips to workers.

This system legally removes employers from the tip distribution chain, eliminating administrative burdens associated with managing traditional tronc arrangements whilst meeting requirements under the Employment (Allocation of Tips) Act 2023. The platform maintains comprehensive digital records of every tip transaction, satisfying the legal obligation for employers to document tip allocation processes transparently.

URocked facilitates direct payments to individual staff members or team-managed pools, ensuring tips are distributed fairly without any deductions beyond statutory tax requirements, guaranteeing employees receive 100% of their gratuities as mandated by law. The automated system eliminates manual record-keeping errors and reduces non-compliance risks by maintaining real-time transparency in tip distribution.

Welcome to the URocked movement

Where cashless tipping meets legal ease and transparency!