Yes, tips are taxable and subject to income tax in the UK. National Insurance Contributions (NICs) depend on how tips are managed. Tips paid directly from customers to employees are taxed under Self Assessment but not subject to NICs. When employers control tip distribution, such as with card or pooled digital tips, PAYE applies for both Income Tax and NICs. Independent tronc systems deduct Income Tax but remain exempt from NICs for both employer and employee.

For self-employed workers, tips count as business income and must be declared in Self Assessment returns, attracting both Income Tax and Class 2 and Class 4 NICs based on total profits. Businesses must operate PAYE for controlled tips and pay employer NICs at 15% on earnings above £5,000 from April 2025. Tips are not subject to VAT as they are voluntary payments, unlike mandatory service charges, which attract 20% VAT. The URocked Tipping App assists workers in recording and reporting tip income to HMRC.

Service charges differ from tips because they are added automatically to bills. Mandatory service charges are taxable for both businesses and employees, while discretionary ones remain outside VAT scope.

Yes, tips are taxable and subject to income tax in the UK. All tips received are classified as employment income under UK tax law, making them liable for Income Tax in all circumstances. For tips received under employer control National Insurance Contributions (NICs) are due for both the employer and the employee. There is no VAT on tips in the UK.

National Insurance Contributions depend on how tips are distributed to staff. Tips paid directly from customer to employee are subject to Income Tax but no National Insurance Contributions. The employee is responsible for declaring these tip earnings to HMRC. Tips under employer control such as card tips added to bills are subject to Income Tax, employee NICs and employers NICs. The employer is responsible for operating PAYE, deducting tax and National Insurance deductions.

Tips distributed through an independent tronc system are subject to Income Tax for employees. For both employees and employers no National Insurance Contributions are due on tips using an independent tronc system.

Yes, tips are treated as business income and are taxable for self-employed workers. Tips received by self-employed individuals form part of their total business income under UK tax law, making them subject to Income Tax and National Insurance Contributions. Self-employed workers must declare all tip income through their Self Assessment tax return to HMRC to ensure compliance with tax obligations.

Tips are subject to Income Tax based on total trading profit after deducting allowable business expenses. HMRC calculates tax liability on the net profit figure, which includes all tip income received during the tax year. Self-employed individuals cannot use the trading allowance to exempt tip income, as tips form part of their regular business activities rather than miscellaneous income.

National Insurance Contributions apply to tip income for self-employed workers through Class 2 and Class 4 contributions. Class 2 National Insurance Contributions are due when total profits including tips exceed £6,725 per year. Class 4 National Insurance Contributions at 9% apply to profits between £12,570 and £50,270, with a 2% rate on profits above £50,270. Both contributions are paid through the Self Assessment system alongside Income Tax.

Tips are subject to income tax in the UK with National Insurance Contributions for employer and employee if tips are under employer control. HMRC applies different taxation based on how they are paid and distributed. Tips received as cash, processed through card payments, paid digitally, distributed via tronc systems, or given as gift vouchers will be subject to different tax obligations.

Cash tips are tips paid directly to employees by customers using physical money. When employers have no control over cash tip collection and distribution, employees must record and declare all amounts through Self Assessment tax returns. HMRC collects tax on cash tips through the Self Assessment system, requiring employees to pay Income Tax at rates of 20%, 40%, or 45% based on total annual earnings. When employers control cash tip distribution through payroll systems, tax collection occurs via PAYE with automatic Income Tax and National Insurance deduction.

Card tips are tips processed through electronic payment systems using credit cards, debit cards, digital wallets and contactless payments. Card tips are typically under employer control as they are processed through the businesses payment systems. Employers are responsible for deducting tax from card tips through the PAYE system before distributing payments to employees. PAYE (Pay As You Earn) is the system employers use to deduct Income Tax and National Insurance contributions directly from employee earnings at source.

Card tips face automatic Income Tax deduction at 20%, 40%, or 45% rates depending on the employee’s total earnings bracket. National Insurance contributions are deducted simultaneously at Class 1 rates through the same PAYE process.

Digital tips are tips paid directly to employees through mobile payment applications, online platforms, or designated payment terminals. Employees receiving digital tips paid directly by customers outside of employer control must record and declare all amounts through Self Assessment tax returns. These tips are treated like cash tips. HMRC collects tax on digital tips through the Self Assessment system, requiring employees to calculate and pay Income Tax at standard rates of 20%, 40%, or 45% based on total annual earnings.

Digital tips collected and distributed under employer control in a system such as a team tip pool, the employer is responsible for deducting tax and NICs through the PAYE system.

Tronc tips are gratuities collected and distributed through a formal pooling arrangement managed by an appointed troncmaster. A tronc is an independent system for collecting and distributing tips fairly amongst staff members. A troncmaster is the person legally responsible for operating the tronc system and ensuring tax compliance. The troncmaster bears responsibility for deducting Income Tax through PAYE before distributing tips to employees. Income Tax applies at standard rates of 20%, 40%, or 45% based on each employee’s total earnings, with automatic deduction through the tronc’s PAYE system.

Gift vouchers are non-cash gratuities provided by customers in the form of store credits, meal vouchers, or retail gift cards. Employees receiving gift vouchers as tips outside of employer control must record and declare the monetary value of the voucher. The monetary cash equivalent of these tips are taxable as employment income. No NICs are due on the monetary value of the gift voucher. For gift vouchers under employer control the monetary value must be reported via PAYE and subject to income tax and NICs.

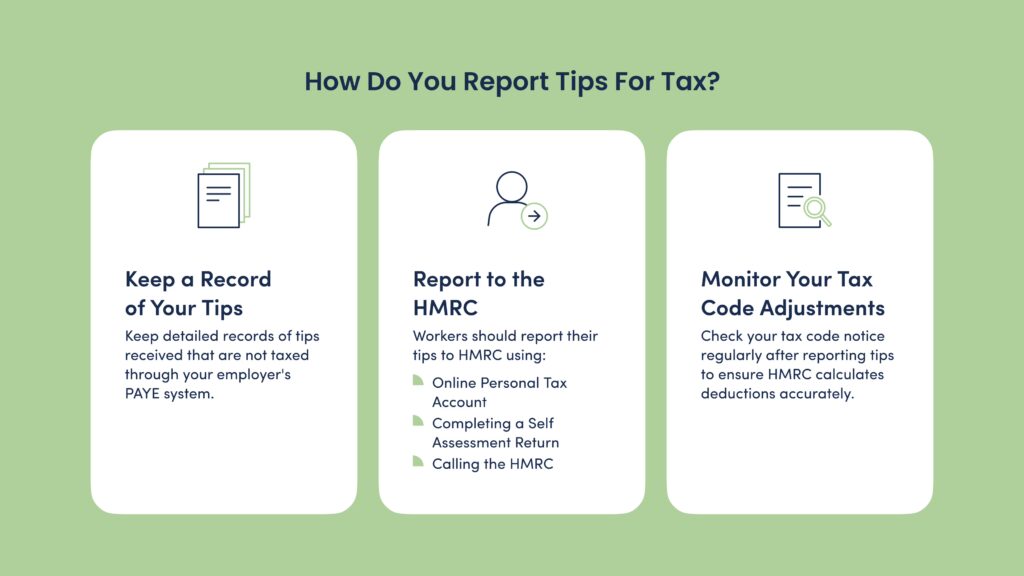

To report tips for tax, employees must complete a self assessment tax return. For tips received from their employer this is automatically reported via PAYE. Below are the steps for reporting your tips for tax:

1. Keep a Record of Your Tips

Maintain detailed documentation of all tips received that are not already taxed through your employer’s PAYE system. Track the total amount using a logbook or digital system to ensure accurate income reporting.

2. Report to the HMRC

Report your tips to HMRC using an appropriate reporting method based on your preference. Workers have the option of reporting tips to HMRC with the three options below:

3. Monitor Your Tax Code Adjustments

Check your tax code notice regularly after reporting tips to ensure HMRC calculates deductions accurately, especially when tip amounts change significantly. Verify that your employer deducts the correct tax amount from regular wages following any tax code modifications. Contact HMRC immediately if discrepancies arise between reported tip income and actual tax code adjustments to maintain compliance and avoid underpayment penalties.

Use the URocked Tipping App to record tips for tax purposes. URocked Tipping App provides a comprehensive digital solution for tracking all tip income required for HMRC compliance and Self Assessment declarations.

URocked Tipping App offers several features that make it an excellent choice for tip recording. The app maintains a user-friendly interface that simplifies the process of logging tip amounts throughout the working day. All digital tips received directly from customers or as part of pooled arrangements are automatically recorded within the system. The tipping app captures essential transaction details including dates, amounts, payment methods, and tip sources for complete audit trails. URocked Tipping App ensures compliance with UK tax law by maintaining records in formats acceptable to HMRC for Self Assessment reporting. The platform generates easy-to-export reports that streamline the Self Assessment process, reducing the administrative burden of manual tip calculation and declaration.

Yes, cash tips should be declared to the HM Revenue and Customs (HMRC). Tips are taxable income and must be reported regardless of how they are received. Workers who receive cash tips must report tips through a Self Assessment tax return, through their personal tax account online or by calling the HMRC. For cash tips received directly from a customer, the employee is personally responsible for reporting this income to HMRC. Cash tips collected by the employer, the responsibility for reporting and deducting tax falls to the employer via the PAYE (Pay As You Earn) system.

Tips are not taxable as business income, are not subject to VAT but are subject to employers’ National Insurance Contributions on tips if they are under employer control. Tips belong to employees as additional compensation for their services and do not form part of business revenue or profit calculations. All tips that are received where the employer has significant control in how tips are distributed are employer controlled tips. All tips under employer control are subject to employers National Insurance Contributions. Employers must pay employer National Insurance Contributions at 15% on earnings above £5,000 per year from 6 April 2025. These earnings include workers salaries and tips they receive as part of their job.

Businesses are responsible for operating PAYE (Pay As You Earn). Businesses receiving tips must process these amounts through their payroll system and deduct Income Tax and National Insurance Contributions via PAYE before distributing tips to staff.

Businesses can utilise a tronc system managed by an independent troncmaster to distribute tips, which exempts these payments from National Insurance Contributions whilst still requiring Income Tax deduction via PAYE. This arrangement provides significant cost savings for businesses whilst ensuring compliance with both tax obligations and the new legal requirements for tip distribution.

No, there is no VAT on tips. Tips remain outside the scope of VAT because they constitute voluntary payments from customers rather than charges for services. HMRC treats tips as gratuities given freely by customers to recognise service quality, not as fees for specific business services.

VAT applies to business transactions where payment is made for goods or services. Tips do not form part of the business transaction between the establishment and the customer. The voluntary nature of tips distinguishes them from service charges, which businesses add to bills and may attract VAT. Customers give tips directly to staff members as personal recognition for service quality, creating no VAT liability for the business or employee.

Yes, there is VAT on mandatory service charges at the standard rate of 20% for VAT registered businesses. Mandatory service charges most commonly apply in the hospitality industry such as restaurants, hotels, cafes and other service industries. This is not to be confused with property service charge. For discretionary service charges in the hospitality industry VAT does not apply.

Service charges differ from tips because businesses impose them automatically on customer bills. Businesses include service charges in their VAT calculations and remit the tax to HMRC through regular VAT returns. Customers pay VAT on service charges as part of the total bill amount, unlike voluntary tips which remain outside VAT scope.

Yes, service charges are taxable and subject to income tax for employees in the UK. All service charges received by workers are classified as employment income under UK tax law, making them liable for Income Tax in all circumstances. Service charges controlled and distributed by the employer are subject to employee National Insurance Contributions (NICs). The employer operates PAYE and deducts tax and National Insurance contributions before distributing payments to staff.

Service charges distributed through an independent tronc system follow different tax rules. Employees pay Income Tax on service charge payments from independent tronc arrangements. Employees do not pay National Insurance Contributions on service charges distributed through independent tronc systems.

Workers must declare all service charge income to HMRC regardless of the distribution method. For employer-controlled service charges, this is typically handled through PAYE. Service charges paid directly from customers to employees without employer involvement are subject to Income Tax only. The employee bears responsibility for reporting these payments and paying the appropriate tax.

Yes, mandatory service charges are taxable for businesses and subject to VAT at the standard rate of 20% for VAT registered businesses. Businesses that distribute service charges via payroll must pay employer National Insurance Contributions at 15% on earnings above £5,000 per year from 6 April 2025. Businesses with an independent tronc do not pay employer National Insurance Contributions as service charges do not come under employer control.

The Employment (Allocation of Tips) Act requires all service charges net of statutory tax to be passed directly to staff. VAT is deducted from mandatory service charges with the net-of-VAT amount passed to staff. Service charges passed directly to staff do not create taxable profit for the business. HMRC treats mandatory service charges as business income and an equal expense, resulting in no Corporation Tax liability. Mandatory service charges are recorded on the tax return but create no Corporation Tax impact.

No, a service charge is not the same as a tip. A service charge is a fee added to the bill of a business. The main difference between a service charge and a tip is that a tip is a voluntary payment made at the customer’s discretion. Service charges are mandatory or discretionary. A mandatory service charge is a fee added to the bill where there is an obligation to pay. A discretionary service charge is a fee added to the bill that the customer can choose to pay or not to pay.

Welcome to the URocked movement

Where cashless tipping meets legal ease and transparency!